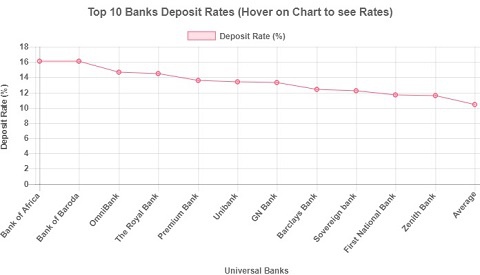

This is a brief presentation of the top 10 banks that pay most on deposits as well as the top 10 Banks with low lending rates.

These are figures released by Bank of Ghana (BOG) in November 2017 with estimates from Savings & Loans and the Microfinance Sector.

The Monetary Policy Committee (MPC) meets on Tuesday, 21 November to determine how the year ends.

The committee may be expected to maintain the current rate of 21% to the end the year.

The Average Interest (AI) rates on deposit by these banks are all above average as these were the top 10 out of the 31 banks.

However the lower tier banks, that is, Savings & Loans and Microfinance companies would generally offer more to reward clients for the higher risk profile they carry.

A depositor could expect above 15% of deposit interest from a Savings & Loans or from a deposit-taking Microfinance.

However, if a depositor seeks to tie up money for a longer time, it would be worth speaking to the bank for other more rewarding returns. E.g. some banks have investment subsidiaries where instruments like unit trusts and fixed deposit exist.

The bank customer should not only look at rates to choose a bank to save with.

Customers should additionally look at speed of service, credibility of bank, accessibility to the funds when needed even when investment is not matured. Customers should always look beyond just rates.

The Annual Percentage Rate (APR) is the real cost of borrowing.

This usually includes other costs apart from the interest rate. For a borrower other factors like ease of access to the funds, time it takes to process requests, some possible hidden charges either at the onset or within the travel time of the facility should all be considered.

Note that the rates for consumer or household borrowing is mostly different or slightly higher than loans for business purposes.

Though the policy rate has declined by 4.5% since the beginning of the year to 21%, the average lending rate for consumer loans has only declined by 1.5% to 31.8%.

This is to be expected as there are more factors other than the policy rate that drives a bank’s lending rates and banks are quick to play on those factors to justify the non-commensurate rate movements.

The customer, therefore, needs to know what they want, have information about it and use the information to their benefit in negotiating for good deals and even changing banks if necessary.

Business News of Friday, 24 November 2017

Source: ghanatalksbusiness.com

Check the top 10 Bank deposit/lending rates

Bank of Ghana

Bank of Ghana